New Delhi [India], June 19: India’s digital payments revolution, powered by the Unified Payments Interface (UPI) and a rapidly expanding base of digital wallet and Prepaid Payment Instrument (PPI) users, has made small-value, app-based payments a part of everyday life for hundreds of millions of Indians. Digital wallets are now used for everything from daily commute and grocery payments to recharges, bill payments and merchant transactions, making the balance and transaction limits attached to them a matter of direct, practical interest to consumers.

Against this backdrop, the Reserve Bank of India (RBI) in April 2026 released a draft Master Direction on Prepaid Payment Instruments (PPIs), 2026, for public comments, replacing its August 2021 framework, with the consultation window open till May 22, 2026. While the draft raises the maximum outstanding balance for Full-KYC wallets to ₹2 lakh, it also proposes to sharply cut the monthly cash top-up limit for such wallets from ₹50,000 to ₹10,000, introduces a uniform ₹25,000 monthly cap on person-to-person transfers, mandates UPI and card-network interoperability, requires immediate refunds for failed transactions and imposes tighter compliance norms on issuers, citing rising fraud and anti-money-laundering concerns.

The proposed reduction in how much money can be loaded into and moved through digital wallets has drawn considerable attention from users and industry alike, with many arguing that genuine, everyday users could be inconvenienced even as the changes do little to deter determined fraudsters. To understand how digital wallet users view these limits, LocalCircles conducted a large survey seeking their direct opinion on whether the RBI should reduce, retain or increase wallet limits, and how a reduction would affect them.

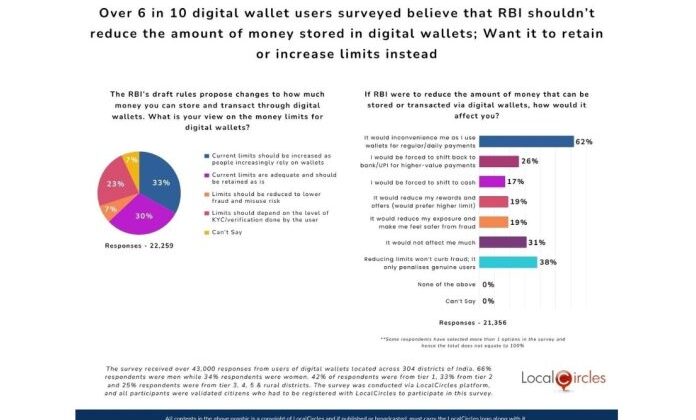

The survey received over 43,000 responses from users of digital wallets across 304 districts of India and found that an overwhelming majority of digital wallet users are against any reduction in wallet limits. 63% of those surveyed want the RBI to retain or increase limits, only 7% support reducing them, and 23% believe limits should depend on the level of KYC/authentication done by the user. Further, 62% say they would be inconvenienced if limits were reduced, and 38% believe that reducing limits will not curb fraud, but instead penalise genuine users. The detailed findings are summarised below.

63% of digital wallet users surveyed believe RBI should retain or increase limits; 23% believe limits should depend on level of KYC/authentication

With the RBI’s draft rules proposing changes to how much money can be stored and transacted through digital wallets, the survey first sought users’ view on the money limits for digital wallets. In response, 33% said current limits should be increased as people increasingly rely on wallets, while 30% said current limits are adequate and should be retained as is – taking the share that wants limits retained or increased to 63%. Another 23% felt limits should depend on the level of KYC/verification done by the user, and only 7% said limits should be reduced to lower fraud and misuse risk, while 7% could not say. This indicates that a large majority of users see digital wallets as a growing necessity rather than a risk to be curtailed. This question in the survey received 22,259 responses.

62% of digital wallet users surveyed believe that they would be inconvenienced if RBI reduced the amount of money that can be stored or transacted via digital wallets; 38% also believe reducing limits won’t curb fraud but penalise genuine users

The survey next asked digital wallet users how it would affect them if the RBI were to reduce the amount of money that can be stored or transacted via digital wallets. In response, 62% said it would inconvenience them as they use wallets for regular/daily payments, 26% said they would be forced to shift back to bank/UPI for higher-value payments and 17% said they would be forced to shift to cash. Among the respondents, 19% felt it would reduce their rewards and offers, another 19% felt it would reduce their exposure and make them feel safer from fraud, 31% said it would not affect them much. Importantly, 38% of users stated that reducing limits won’t curb fraud and will only penalise genuine users. This question in the survey received 21,356 responses. (Some respondents selected more than one option and hence the total does not equate to 100%.)

To summarise, the survey makes it clear that digital wallet users overwhelmingly do not want the RBI to reduce the amount of money that can be stored or transacted via digital wallets. With 63% of users wanting limits retained or increased and only 7% in favour of a reduction, the message from consumers is that digital wallets have become an everyday financial tool rather than a fringe convenience. As wallet usage deepens across tier 1, tier 2 and smaller towns, users appear to view higher or stable limits as essential to managing their daily payments seamlessly.

The concern around the proposed reduction is rooted in real-world impact. 62% of users say a reduction would inconvenience their regular payments, while sizeable proportions say they would be pushed back to bank/UPI for higher-value payments (26%) or even to cash (17%) – an outcome at odds with the broader push towards a digital, less-cash economy. With 38% of users asserting that lower limits won’t curb fraud and will only penalise genuine users, there is clear scepticism about whether reducing limits, particularly the sharp cut in monthly cash top-up from ₹50,000 to ₹10,000 proposed in the draft PPI Directions, will achieve its stated objective.

LocalCircles will be escalating these survey findings with the RBI and other stakeholders as part of the public consultation on the draft Master Direction on Prepaid Payment Instruments, 2026. While users broadly welcome measures that improve security, interoperability and faster refunds, the survey suggests that the central bank should reconsider any reduction in wallet storage and transaction limits, and instead consider retaining or increasing them – potentially linking higher limits to the level of KYC/authentication completed by the user, an approach 23% of users have endorsed.

Survey Demographics

The survey received over 43,000 responses from users of digital wallets located across 304 districts of India. 66% respondents were men while 34% respondents were women. 42% of respondents were from tier 1, 33% from tier 2 and 25% respondents were from tier 3, 4, 5 & rural districts. The survey was conducted via LocalCircles platform, and all participants were validated citizens who had to be registered with LocalCircles to participate in this survey.

About LocalCircles

LocalCircles, India’s leading Community Social Media platform enables citizens and small businesses to escalate issues for policy and enforcement interventions and enables the Government to make policies that are citizen and small business centric. LocalCircles is also India’s # 1 pollster on issues of governance, public and consumer interest. More about LocalCircles can be found on http://www.localcircles.com

Media Contact: media@localcircles.com, +91-8585909866